11.06.13

Posted in Globalstar, Inmarsat, Iridium, LDR, Operators, Orbcomm, Services at 11:02 am by timfarrar

In my view the announcement of a partnership between Orbcomm and Inmarsat on Monday evening may represent a sea change for the MSS industry, as Orbcomm showed how its planned “multi-network operator strategy” could eventually lead to it getting out of the business of operating its own satellite fleet, allowing Orbcomm to be what it wants to be: a solutions provider rather than a satellite operator.

In the short term the deal means that Orbcomm will invest in developing a new low cost Inmarsat ISatDataPro (IDP) module, costing around $100 (i.e. aiming to be less expensive than Iridium’s SBD module) which OEMs and VARs can choose to drop into their terminals as a direct alternative to Orbcomm’s own OG2 module, using a common management interface provisioned by Orbcomm.

The choice of module will be up to the OEM, and will depend on their data needs (IDP has higher capacity and less latency, because there will sometimes be several minute gaps in coverage between the 17 OG2 satellites), the geographies they will serve (Inmarsat will provide access to Russia and China) and the price they are willing to pay (IDP service will be more expensive than the current Orbcomm $5-$6 OEM ARPUs). Note that this is somewhat different than Orbcomm’s arrangement with Globalstar, under which Orbcomm’s Solutions business offers a Globalstar tag to retail customers (and existing Comtech VARs), but Globalstar will not be a direct alternative for Orbcomm’s OEM customers (who buy from Orbcomm’s Devices and Products business).

In the longer term it seems to me that (although this is not part of the current agreement with Inmarsat) Orbcomm will very likely not build a third generation of LEO VHF satellites, as the nature of their network (where the LEO satellites search actively for channels that are free of interference as they orbit the Earth) would be very difficult to consolidate onto an Inmarsat GEO platform. Because Orbcomm will have access to Inmarsat capacity on an I6 constellation which will last into the 2030s, eventually (in a decade or more) Orbcomm could instead migrate its customer base onto Inmarsat’s L-band services, so that it will not have to spend hundreds of millions of dollars on another round of fleet replenishment. In fact, if Orbcomm has any substantial launch problems with OG2 (remember that the satellites from its last two launches have been lost) it might not even make sense to reinvest the insurance proceeds in replacement satellites and conceivably such a migration could take place more quickly.

The significance of this announcement is that it appears to represent the first step towards a reduction in the amount of capex being invested in the rather slow growing MSS market. The next question will be whether, when Inmarsat orders its I6 L-band satellites (likely in late 2014 or early 2015), it opts for a copy (or even a simpler version) of the I4 constellation, and thus whether, as I suggested last year, we really have now reached the “end of history” in the MSS L-band industry. After all, with the sale of the Stratos energy business to RigNet (and a likely disposal of Segovia), Inmarsat is now backing away from its strategy of going direct, and is continuing to focus on maritime price rises to boost revenues, in accordance with the other part of my “end of history” thesis.

Permalink

10.21.13

Posted in Financials, Globalstar, Handheld, Inmarsat, Iridium, LDR, Maritime, Operators, Services at 9:33 am by timfarrar

I won’t belabor the errors of physics in the movie, instead just noting that even though you might think that in space things can keep going in a straight line indefinitely, they are still subject to gravity and you can’t get to a higher orbit without some form of propulsion.

We’ve now seen confirmation from Iridium of what I pointed out last week, that Q3 was very bad for the MSS industry. Iridium missed its expectations for equipment revenues (i.e. handset sales) and subscriber growth (i.e. M2M net adds), although at least the government contract renewal is more favorable than expected – the unlimited nature of the contract removes the incentive for the DoD to scrub its user base to remove unused handsets, which has been a headwind for Iridium in the last couple of years.

Its far from clear that anyone else is doing better: it looks like Iridium’s competitors also saw pretty poor handset sales in Q3 and the SPOT 3 has been very slow to arrive in stores as well. Moreover, the government business is dire – Intelsat’s profit warning (which included its off-net business reselling MSS) is a bad sign for Inmarsat, as are the large scale layoffs in Astrium’s government business last week.

Inmarsat has now followed up its promise not to raise FleetBB prices in 2014 with an enormous 48% rise in maritime E&E prices from January, in an attempt to sustain maritime revenue growth next year. While the stated intention is to persuade the remaining pay as you go customers to move off the E&E network and choose FleetBB instead, the vast majority of higher spending B and Fleet customers have already migrated and many of the remaining users are mini-M voice-only users or really want the PAYG service because they are only occasional users, so FleetBB is not necessarily the ideal option.

Inmarsat is clearly calculating that these customers won’t want to risk moving to Iridium after the OpenPort problems earlier this year and has stepped up its efforts to portray Iridium’s network as “failing”. Despite all this, no-one believes that Inmarsat could possibly achieve its 8%-12% revenue growth target for 2014 and I expect this to be “softened” in the near future as well. Inmarsat is also likely to emphasize its opportunities for internal cost savings next year and move to dispose of some retail business units like Segovia.

Its interesting to speculate about implications for the wider satellite industry as well. Last time around (in 1999-2003), problems in the MSS industry were a harbinger of a downturn in the FSS industry a couple of years later. That came in the wake of a peak in satellite orders in the 1999-2001 timeframe and after the launch of these satellites, which resulted in a sharp decline in prices, the FSS industry took a big hit. We’ve seen a similar peak in orders in recent years (2009-10), and while the major operators are much more likely to retain pricing discipline (in a far more consolidated industry than a decade ago), the advent of High Throughput Satellites, especially those owned by smaller players like Avanti (who might become the most desperate for contracts), could pressure prices in certain market segments and geographies.

Just as an example, in recent years, underlying transponder demand has grown at roughly 4% p.a., but revenues have been boosted by around 2% p.a. by price rises. Even if demand growth continues (not a foregone conclusion in some sectors like government where WGS is an alternative), a reversal of the pricing trend would certainly make a big difference to the FSS revenue outlook. As I said at the beginning of this post, gravity clearly exerts a force, even in space.

Permalink

10.14.13

Posted in Financials, Globalstar, Government, Handheld, Inmarsat, Iridium, LDR, Operators, Orbcomm, Services at 10:03 am by timfarrar

Incredible…it’s even worse than I thought

That’s been the reaction to my 57 page Globalstar profile, released on Friday (you can see the contents list here and get an order form here), because of the history of challenges that the MSS industry has faced in the past and more particularly the difficulties that the industry is seeing this year.

After discussions with a number of people in the industry over the last few weeks, it looks like Q3 has been pretty disastrous for MSS sales across the board, with none of the usual surge in demand expected in the summer months, as customers stock up to prepare for outdoor adventures or potential hurricanes. Part of that relates to slow government orders, as a result of the sequester (predating the current shutdown), but commercial demand has also been poor, and that’s much harder to explain.

In the handheld segment, one suggestion is that Hurricane Sandy proved that terrestrial cellphone networks are now considerably more reliable during disasters (and far more data capable than MSS phones), so companies are no longer giving as high a priority to MSS equipment in their disaster planning. In the M2M segment, a fairly convincing explanation is that service providers who formerly specialized in MSS are now focusing more and more on selling cellular-based solutions to customers who find they don’t need MSS as a backup.

As a result, I’m now convinced that subscriber growth (and equipment sales) will fall short of expectations this year, particularly in the handheld and M2M segments, for almost all of the major MSS players, with knock-on effects for subscriber revenues in Q4 and more particularly next year. The defense business also looks poor (as shown by Intelsat’s recent profit warning): the word on the street is that Inmarsat may dispose of its Segovia government FSS business, as revenues in Inmarsat’s US Government business unit fell by 11% year-on-year in the first half of 2013 and appear to have eroded further in recent months, particularly in Segovia’s VSAT business. The sale price would be a fraction of what Inmarsat paid for Segovia, but in exchange Inmarsat would hope to secure a GX airtime contract, similar to its RigNet deal in the energy sector.

In the case of Globalstar, the implications of the MSS downturn are that while Globalstar should be able to meet the new bank case revenue forecasts, it won’t be easy to beat them. However, unlike some other players, Globalstar is fortunate in having the potential upside from monetizing its spectrum, if it can complete a deal with Amazon or another company. The report looks at spectrum valuation for both LTE and TLPS and concludes that there could be substantial value for Globalstar, although realizing this will require both rapid approval from the FCC and for a deal to be struck fairly quickly, before new spectrum bands such as 3550-3650MHz develop an alternative ecosystem at what will likely be much lower prices. If you are interested in getting a copy, please contact me for more details.

Permalink

09.19.13

Posted in Financials, Globalstar, Handheld, Inmarsat, Iridium, Operators, Regulatory, Services, Spectrum at 9:32 am by timfarrar

Why didn’t Phil think of this first?

With MSS revenues in a bit of a funk this year, its not surprising that MSS operators are pursuing opportunities to attract consumers and expand the voice market outside the traditional verticals. We saw this first of all with Thuraya’s SatSleeve, announced at the Satellite 2013 conference in March. The SatSleeve connects via Bluetooth (and in the latest version WiFi) to an iPhone allowing the customer to use their iPhone contacts and touch screen interface. However, a key limitation is the need for compatibility of the sleeve with a particular phone form factor, and Thuraya has just launched a new version of the SatSleeve compatible with the slightly larger iPhone 5 handset rather than the original iPhone 4.

One way to overcome this handset compatibility issue is to use an external puck-like device, similar to a SPOT Connect or DeLorme inReach product, but offering voice and data capability in addition to simple messaging. This concept has been around for many years, and indeed was part of Craig McCaw’s new business plan when he bought ICO out of bankruptcy back in 2000: ICO told the FCC in its original ATC application in March 2001 that

“The use of already-permitted wireless technology such as Bluetooth or IEEE 802.11 could allow a whole range of consumer devices – standard terrestrial phones, PDAs, or laptop computers – to communicate with a satellite transceiver that houses the antennas, amplifiers, and other electronics unique and specific to the satellite link”.

Subscribers to my MSS research service heard 6 weeks ago about Iridium’s new handheld product, scheduled for launch at the end of the year, which is apparently exactly this puck-like device. It will be positioned to compete at the low end of the handheld market with a broadly comparable price to Thuraya’s SatSleeve (which was originally announced at $499 but is now selling for $599 to $799) and the Inmarsat and Globalstar handheld phones. I’m now told that Inmarsat is working on a similar device for release towards the end of next year, and meanwhile Globalstar has announced that it is “aiming to bring a $100 satellite device to market in 18 months time…to enter into a totally different market”.

I understand that Globalstar’s new device is likely to be the long-awaited two-way SPOT product, and may not be voice-capable like Iridium and Inmarsat’s new devices. It remains unclear whether the form factor will be a smartphone-connected puck (like SPOT Connect) or a standalone device: certainly the standalone device has sold much better for Globalstar to date, but equally well this might make it harder to expand beyond the current market of techie-focused backpackers and outdoorsy people (the vast majority of SPOT users are like me: 40-something relatively high income males with an interest in technology). Given the 18 month timetable stated by Globalstar, its also unclear whether this would be based on the new Hughes chipset or the current SPOT uplink plus a similar downlink channel, as the second generation ground segment upgrades are supposed to take about two more years to complete.

As Globalstar moves to raise its profile with investors, it seems the next stage will be a new round of fundraising (Globalstar noted in its 2013Q2 10-Q that “In June 2013, the Company entered into an agreement with Ericsson which deferred to September 1, 2013 or the close of a financing approximately $2.4 million in milestone payments scheduled under the contract”), presumably helping to reduce some of Thermo’s $85M backstop commitment (of which $40M had been provided by the end of July and $4.4M had been offset by receipts from termination of the 2009 share lending agreement). Indeed, it would be plausible for fundraising to go beyond this ~$35M level given the rise in Globalstar’s share price in the expectation of a positive outcome from the FCC, though it appears unlikely Globalstar will order more satellites anytime soon, given that the legal disputes with Thales are apparently still ongoing (Thales has “alleged that Thermo had failed to pay Thales $12,500,000 by December 31, 2012 as required by the Settlement Agreement“).

It seems Globalstar is highly confident that its NPRM will be issued by the time Chairman Clyburn leaves office, so it would be reasonable to suspect that this new financing is intended to take place in the next month or so, helping to cover payments of $20M+ due to Hughes between August 2013 and January 2014). Last week’s grand bargain over the 700MHz A&E blocks, DISH’s AWS-4 downlink waiver request and the H block auction, certainly indicates that I was too pessimistic in believing that Clyburn didn’t want to address spectrum issues and would leave these for Wheeler, and it would therefore now not be in the least bit surprising to see the Globalstar NPRM released at or around the time of the September FCC Open Meeting (when Clyburn will have what might be the last chance to trumpet her accomplishments as Chairman). Clyburn also appears less likely than Wheeler to pursue the “harm claim threshold” approach favored by the FCC’s TAC, which is good news for Globalstar in terms of how long it would take to issue an FCC order, although given that the FCC highlighted the speed with which it had moved to complete the DISH ruling last December (within 9 months of issuing the NPRM), it is still hard to imagine a final ruling on TLPS before early summer 2014.

So the key issues for Globalstar are likely to be how successfully it can build up its MSS business (note that the revenue projections given for the bank case in the new COFACE agreement generate just enough cash to cover debt, interest and capex payments through 2022 but little else) and more importantly whether Globalstar can find a partner to exploit its spectrum assets. We know about Amazon, but will there be other interest either from the cellular industry or (perhaps more plausibly) from non-traditional players? What are the best comparisons for spectrum valuation for TLPS and/or LTE authorization? I’ll be publishing my updated profile of Globalstar shortly and all of these issues will be discussed along with my revenue projections for the MSS business.

Permalink

09.09.13

Posted in Aeronautical, DISH, Financials, Globalstar, Inmarsat, Iridium, LightSquared, Operators, Orbcomm, Regulatory, Spectrum at 3:12 am by timfarrar

That seems an appropriate title, as I head off to London and Paris this week, to hear MSS and other satellite operators talk about their future opportunities. I found it interesting to note that Euroconsult released their updated MSS market assessment a couple of weeks ago, cutting their projection of future wholesale revenue growth from 7% p.a. (in the previous version of their analysis) to 5% p.a. over the next 10 years, getting back much closer to my forecasts from a couple of years ago.

However, by my estimate, MSS wholesale service revenues only grew at 2% in 2011 and 3% in 2012 (not 5% as Euroconsult estimates, perhaps due to double counting of Orbcomm’s revenue growth from resale of Inmarsat and now Globalstar services) and the majority of this growth in 2012 came from Inmarsat’s price rises. While it originally looked like 2013 was shaping up to see a bit better growth, Iridium has reduced its guidance, Globalstar’s second quarter results were nothing to write home about and Inmarsat is again seeing a significant part of its modest revenue growth being driven by maritime price rises. So its now far from clear that we will get even to Euroconsult’s lowered 5% growth projection in the near term.

While spectrum is a wildcard that could provide incremental revenues for Globalstar (through a potential deal with Amazon) and Inmarsat (through a resumption of lease payments from LightSquared), progress here may not be as fast as expected. Globalstar’s hoped for NPRM is not on the tentative agenda for the FCC’s September Open Meeting, presumably meaning that although the NPRM has now been placed on circulation this issue may be left for incoming Chairman Wheeler to finalize. The recent application by Oceus Networks for an experimental license to test TLPS for DoD users also suggests that a partnership with Amazon is far from set in stone as the way Globalstar will be able to realize value from its spectrum assets.

In contrast, it looks increasingly like DISH will succeed in its bid to buy LightSquared’s satellite assets later this year, and DISH has agreed to assume the Inmarsat Cooperation Agreement as part of its stalking horse bid. But buying LightSquared is a sign that DISH is unlikely to move forward quickly with its entry into the wireless market, because it would take until late 2014 or beyond before the FCC could approve any change to downlink use for the 2000-2020MHz AWS-4 uplink band. At the moment it seems that interim FCC Chairman Clyburn doesn�t want to take a decision even on LightSquared�s uplink band (let alone address the purported �swap??? of downlink spectrum, which Ergen doesn�t want or need � leaving MAST Capital Management stuck holding a largely worthless lease of the 1670-75MHz spectrum band), because the FCC will not receive reply comments until September 23 (shortly before Clyburn relinquishes the chairmanship). So even if DISH buys the satellite assets, and drops the request to get hold of the 1675-80MHz band, reaching any resolution of the current regulatory issues in the L-band will undoubtedly be a lengthy process.

Charlie Ergen hinted on DISH�s Q2 call that he doesn�t anticipate simply continuing the Cooperation Agreement in its current form, so it would not be at all surprising to see a fight between DISH and Inmarsat over renegotiation of the Cooperation Agreement in the early part of 2014. One possible compromise could be in the form of a partnership between DISH and Inmarsat to use the TerreStar-2 satellite to preserve Inmarsat�s S-band license in Europe, in exchange for further postponement of any cash payments under the Cooperation Agreement.

Despite (or perhaps because of) the challenges that the MSS market faces, M&A continues apace. Recent agreements include Inmarsat�s sale of its energy sector assets to RigNet and Rockwell Collins� acquisition of ARINC. I understand a number of additional notable transactions are in the works. Rumors persist that SITA has put OnAir up for sale (only six months after buying Airbus’s stake in the business) and Honeywell appears to be the most likely buyer, while Orbcomm continues its acquisition of satellite M2M service providers and may now be in negotiations to buy Comtech Mobile Datacom.

UPDATE: According to an OnAir spokesperson “SITA has no intention to sell OnAir to Honeywell or to anyone else and remains OnAir’s sole shareholder.”

It will be particularly interesting to see the valuation put on OnAir, given the recent disastrous public offerings of Gogo and Global Eagle/Row44, because if OnAir attracts a much lower valuation than Gogo and Row44 it could be a sign that SITA is pretty pessimistic about the future of the inflight connectivity market. That would be a surprise to many, because after all inflight connectivity is seen as one of the major areas for growth in the MSS market going forward, but at present making an operating profit, let alone a return on investment, is a pretty distant prospect for most if not all of the service providers. So if now is the time for SITA to get out, will this turn out be the age of wisdom for the sellers and the age of foolishness for the buyers, or the reverse?

Permalink

07.01.13

Posted in Aeronautical, Financials, Services at 1:24 pm by timfarrar

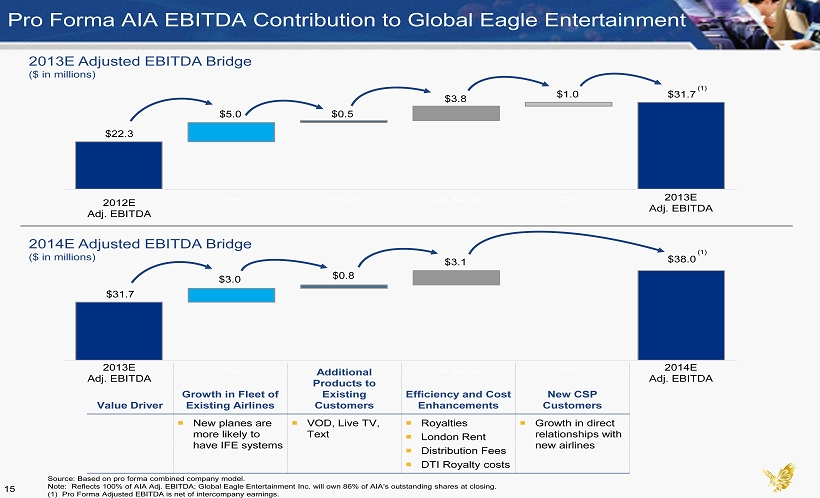

As readers of this blog know, I’ve not been a fan of Row44′s content-focused strategy for inflight connectivity, and I pointed out how ludicrous Global Eagle’s forecasts were last November. However, the meltdown of this strategy has come even sooner than I expected, with today’s announcement that instead of charging for streaming video content on Southwest planes, the service will instead be sponsored by DISH Network and made available for free to passengers, in exchange for watching a 30 second commercial.

The fact that Row44 has struck this deal now, only a few months after launching the inflight TV service, suggests that the paid take-up has been dire (which is hardly a surprise, given the Southwest customer profile, their average flight length and the lack of onboard power outlets). Even worse, according to DISH’s CMO, the sponsorship has no announced end date (although it will run at least through the end of this year), suggesting that instead of being a temporary deal to boost awareness (like Gogo’s Thanksgiving to New Year 2010 free inflight WiFi offer, sponsored by Google), it may never be possible to get many passengers to pay for the service. This move may also be a pre-emptive counter to JetBlue’s plan to offer free inflight WiFi to its passengers, but will do nothing to boost take rates for Row44′s paid internet service, and will more likely undermine them now that Southwest passengers can instead watch video content for free.

The business projections presented by Global Eagle last November (setting out their supposed “highly visible” 2014 adjusted EBITDA forecast) estimated that the TV/VOD/IPTV service would have a take rate of 5.75% and generate $5 per user in 2014 (i.e. $0.29 per passenger opportunity), plus a further $0.15 per passenger in portal services. Although DISH has not revealed its sponsorship payment, according to my calculations based on Gogo’s S-1 filing, Google paid $7M for its 6 week sponsorship, or roughly $0.28 per passenger carried (about $2.50 per Internet session) during the period. Its a safe bet that DISH is paying a lot less than that for an ongoing deal: I’d estimate roughly $1M per month (~$0.10 per passenger carried), or about a third of Global Eagle’s projection for revenues from these services in 2014.

UPDATE (7/1): It was pointed out to me that the sponsorship deal is between DISH and Southwest, so it’s not clear how much of DISH’s sponsorship payments are being passed on to Row44 or indeed if Southwest will be making additional payments to Row44 to subsidize the TV service. That is possible, but its hard to believe that Southwest would want to provide a large subsidy to Row44 for an indefinite duration, when Southwest originally expected to be receiving a share of revenues, just like from inflight WiFi (and when Gogo is offering airlines a ~30% revenue share from its Gogo Vision services).

UPDATE (7/3): Global Eagle confirmed in a press release that “its Row 44 subsidiary has entered into a groundbreaking content and connectivity partnership with its customer Southwest Airlines” or (without the spin), that Row44 has changes the terms of its TV services agreement with Southwest, presumably to a flat fee rather than a revenue share. Undoubtedly this means a reduction compared to Row44′s projected 2014 revenues, although when the next set of financial results come out, look for further spin describing the change as providing a significant boost to revenues in 2013Q3 (compared of course to the near total absence of content revenues in Q2).

Based on Gogo’s published data, revenue from portal services is also going to be vastly less than Global Eagle estimates, while there has also been “an increase in license fees paid for the content delivered to airline customers” (which are unlikely to reduce, even if revenues are lower than expectations) and bizarrely, Global Eagle appears to have ignored any revenue share that may be payable to Southwest in its assumption of a 87% gross margin on content services. By my estimates, even ignoring any negative impact on Row44′s connectivity revenues from the free TV offering, that could leave a $30M to $40M hole in Global Eagle’s projected $75M of adjusted EBITDA in 2014. Put another way, it seems that this business really wasn’t “highly visible” after all.

Permalink

06.12.13

Posted in Aeronautical, Financials at 4:25 pm by timfarrar

Gogo’s IPO roadshow is taking place this week (with completion apparently expected next Tuesday) after the company filed a revised S-1 on Monday June 10 indicating that it is seeking to sell 11M shares at between $15 and $17, giving the company an enterprise value (at the midpoint of this range) of approximately $1.3B (or even higher if you assume, as Gogo does, that the cash it raises needs to be spent on upgrading Gogo’s network to ATG-4, including doubling the number of cell sites by 2015). That seems pretty optimistic given the modest revenues that Gogo generates at present ($235M in 2012) and the losses that the company is making outside its well established Business Aviation segment.

I’ve not yet completed my forthcoming aeronautical communications market report, but I know a lot of people will be looking for some realistic numbers to value the company. So I decided to pull together my detailed estimates for Gogo through 2017, into a 21 page profile and analysis which I’ve published today. You can find a report summary and contents list here, and an order form here. And if you decide to buy my aeronautical market report when its available later this summer, you’ll receive a full credit for the price of the Gogo report.

Feel free to contact me for more details. As a taster, here’s the latest quarterly growth breakdown including 2013Q1. The last quarter is quite significantly short of my estimates, as despite the improving take rate trend line, Gogo took a significant hit on Average Revenue Per Session compared to 2012Q4.

UPDATE 6/13: And here is a comparison with the various analyst forecasts for Gogo which were given out at the roadshow. I’ve left off the names, to spare people’s blushes, but the bank that forecast this to be a $1.6B business in 2017 has clearly been drinking the same Kool Aid as Global Eagle.

Permalink

04.22.13

Posted in Globalstar, Handheld, Inmarsat, Iridium, KVH, Maritime, Operators, Services, VSAT at 9:22 am by timfarrar

Its interesting to note that Inmarsat has been competing much more aggressively against key competitors in the last few months. First, I’m told that Inmarsat offered a bounty to Telemar to capture Anglo Eastern, a key Iridium Open Port customer with 350 ships, from Globe Wireless, in the fourth quarter of 2012.

Then Inmarsat announced in March that Nordic Tankers, one of KVH�s earliest headline customers, was migrating to XpressLink “for enhanced reliability”. Apparently the pricing on that deal is well below the standard list price for XpressLink, but Inmarsat was very keen to demonstrate its ability to take customers away from KVH.

Now (perhaps showing a little pique at losing the recent tender for the AT&T Genus replacement contract) Inmarsat is going after Globalstar, with new North American ISatPhone Pro regional voice plans which will start on May 1, and match Globalstar’s recently announced Orbit and Galaxy plans (though without Globalstar’s “double time minutes” promotional offer). Inmarsat is once again offering a huge bounty to service providers for these new signups, equivalent to multiple months of service revenue.

All of these developments suggest that Inmarsat is determined to seek topline growth in its L-band business and is no longer reluctant (as in the past) to explicitly target its competitors with selective pricing, even though this runs counter to Inmarsat’s recent tendency to increase list prices. Of course, it is less clear whether the new deals will be profitable for Inmarsat, given the incentives needed to achieve these sales.

But with Inmarsat’s investors focused intently on whether the wholesale L-band Inmarsat Global business has returned to growth, and apparently willing to overlook the recent significant contraction in margins within Inmarsat’s Solutions business unit (blamed on a transfer of margin from retail to wholesale operations), that might not matter for now. However, if Inmarsat wants to make more acquisitions (and it is hard to see in the long term who else might end up operating LightSquared’s satellites), then regulators might wonder whether industry consolidation could give Inmarsat even more market power.

Permalink

04.08.13

Posted in Aeronautical, Financials at 10:02 am by timfarrar

No I’m not talking about Intelsat’s current IPO! Although some might raise questions about the company’s debt levels, its also pretty clear that Intelsat’s mobility strategy and its high throughput Epic satellites are the envy of its FSS competitors. What I’m actually referring to is Row44, which went public at the end of January through a merger with Global Eagle, which had raised $190M in a blank check IPO. The end of year results from Row44 and Global Eagle have gone completed unreported, but were filed with the SEC last month, and highlighted just what a disastrous business Row44 really is.

In particular, as installations of the Southwest fleet neared completion, Row44′s revenues in Q4 dropped by 27% compared to Q3 (from $20.1M to $14.8M). Moreover, Row44 only generated total Internet connectivity revenues of $11.4M in 2012 while spending $19.6M on buying bandwidth from Hughes, and produced no revenues from its much ballyhooed content and portal services (despite spending $1.9M on video licensing fees).

In 2013, Row44′s satellite connectivity commitment to Hughes will go up to a minimum of $28M (and more likely well over $30M, because of additional commitments made in early 2013 to add coverage in Russia, and additional trans-Pacific coverage planned later this year). Row44 has also changed its deal with Southwest, so it now only receives fees for passengers using connectivity (between $5 and $6 per user, while Southwest charges $8 for the service), rather than Southwest paying for every boarded passenger under the original agreement, and as part of the new contract, Row44 is adding more capacity, apparently to counter passenger complaints about “slow or restricted services”.

At an investor conference on March 13, Global Eagle’s CFO suggested that paid take rates for other providers “range from high single digits to high teens” and that inferences could be drawn from that for Row44′s take rates on Southwest. Of course that is completely untrue: take rates for Gogo are around 5%, and Global Eagle itself said back in November that the targeted take rate on Southwest was 6.5% in 2014, so its hardly likely that the take rate is higher than that today. I therefore have to wonder if Global Eagle’s CFO actually understands this business at all.

Indeed, the company seems to have a hard time predicting the outlook for its business even in the very short term: this March 13 presentation indicated that the 2012 adjusted EBITDA from Row44 and AIA respectively was -$26M and +$18M respectively, whereas on November 27, 2012, with just one month left in the year, Global Eagle forecast that the full year adjusted EBITDA results for Row44 and AIA would be -$25M and +$22.3M respectively.

If we look forward to 2013, then it seems certain that Row44′s revenues will decline sharply, because of the slowdown in equipment installations (from $61M of equipment revenues in 2012 to ~$35M in 2013, and potentially to only $20M in 2014, based on Row44′s current business plan). More importantly, the company is set to make another significant loss on provision of connectivity services: I estimate $20M-$25M in revenues, depending on the take rates that Southwest achieves, compared to connectivity costs of well over $30M and more likely close to $40M (just in payments to Hughes, ignoring Row44′s own operational costs). In addition, content revenue is still minimal (Global Eagle described the product as “brand new” in mid March), with a very limited selection available, and by my estimate content and portal revenues will be no more than ~$5M this year.

In the longer term, Row44′s new deal with Southwest has locked the airline into a deeply unfavorable competitive position vis-a-vis JetBlue, who intend to offer Internet access for free. Southwest can’t possibly do the same, if they have to pay Row44 at least $5 for every passenger who uses the service, despite the two airlines competing very actively on other passenger amenities (like free checked bags). Moreover, if Row44 is ever to break even, it may have to cut back on the amount of capacity it buys from Hughes (rather than boosting capacity as Southwest currently plans), making Southwest’s Internet service even less attractive compared to JetBlue, which uses much cheaper Ka-band capacity.

In recent days, we’ve seen yet another report predicting rapid growth for in-flight connectivity deployment and revenues. However, none of these reports have got to grips with the issue of what services can be profitable for providers but still affordable for the airlines. Of course, if there’s one lesson to be learned from the Connexion-by-Boeing debacle, its that you can’t just assume companies will be able to continue providing service at an enormous loss indefinitely. After scraping through 2012, raising money at effective interest rates of up to 421%, Row44 has escaped for the time being by capturing Global Eagle’s cash balance. Perhaps unsurprisingly, given its management’s apparently tenuous connection to reality, Global Eagle now intends to “use its balance sheet” to pursue consolidation of the in-flight connectivity business, which might provide some relief from Row44′s current unsustainable business model, but on the other hand may simply drag down other companies in the sector.

We’ll be publishing our own detailed report on the in-flight connectivity business next month, which takes a very different approach to the analyses we’ve seen so far: instead of simply projecting how many planes might be fitted out with each technology, we’ll look at both the revenue and cost base of the various IFC providers, and discuss which of them may be able to find a sustainable long term business model.

Permalink

02.21.13

Posted in Aeronautical, Financials, Government, Inmarsat, Iridium, Maritime, Operators, Services, VSAT at 1:57 pm by timfarrar

As Inmarsat approaches its end of year results presentation, scheduled for March 7, the company’s stock price has been surging in the expectation of continued strong progress in the maritime market, which is likely to lead to full year wholesale MSS revenue growth for 2012 (excluding LightSquared payments) somewhat above Inmarsat’s 0%-2% target. This has been driven primarily by Inmarsat’s 2012 price rises, which have been so successful that Inmarsat announced further price rises of around 10% for E&E services last month.

I estimate that these new price rises could boost wholesale maritime revenues by a further $10M (roughly 3%) in 2013, on top of the pull-through from the mid year price rises in 2012, and as a result, it is plausible to imagine that Inmarsat’s wholesale MSS maritime revenues might rise by as much as 10% in 2013. Thus, unless there are severe cutbacks in government usage this year, overall revenue growth for 2013 may again come in quite a bit above the 0%-2% target. Our updated profile of Inmarsat provides full details of our forecasts by product, and will be released shortly.

That revenue upside perhaps explains why Inmarsat has become notably more aggressive in recent weeks, for example telling its sales team that commission will no longer be paid for selling Iridium products and services (historically Stratos has sold over $10M of Iridium equipment each year). In addition, the IS-27 launch failure appears to have given Inmarsat more confidence that potential partners will need GX for maritime and aeronautical services, rather than continuing to rely on Ku-band services in what may now become a capacity-constrained North Atlantic Ocean Region over the next couple of years.

One intriguing issue to watch in terms of Inmarsat’s relationships with its distributors is the ongoing dispute in Russia, where I’m told Morsviazsputnik has refused to pay for Inmarsat capacity for a substantial period of time (note that Inmarsat’s trade receivables have been increasing by about $10M per quarter during 2012, excluding LightSquared payments), unless all Inmarsat-equipped vessels going into Russian waters use a Russian SIM. This dispute has apparently extended to the Russians modifying their call routing gateway (which sends all traffic within 200 miles of Russian territory to an intercept point in Russia) to give them the ability to cut off the communications on foreign vessels. I’m told that in response Inmarsat has considered terminating the routing of traffic to the Russian intercept point, which would of course escalate the dispute even further and make it even more difficult to recover the withheld revenues.

Beyond this year, Inmarsat is guiding that its 8%-12% revenue growth in 2014-16 will be backend loaded, and so growth in 2014 will not need to increase sharply (which would be difficult prior to achieving global GX coverage). Indeed, a combination of continued price rises on L-band services and a release of some of the cash previously received from LightSquared (and never spent on installing filters) could help to meet expectations in the next few years, even if GX does not live up to Inmarsat’s projected $500M in wholesale revenue by 2019.

With respect to GX, I have been cautious about the $500M target because I have always assumed that maritime would account for the largest share of the GX business and it is very hard to see how Inmarsat could hope to generate $200M-$300M of wholesale maritime GX revenues by 2019, when Inmarsat itself estimates that only $145M was spent on maritime FSS space segment capacity in 2010.

However, I understand that Inmarsat is now suggesting that the GX government business will generate more revenue than the maritime market. Of course that is much harder to prove or disprove, especially as Inmarsat gave very little insight in the October 2012 investor day into whether the government business is expected to rely mainly on the dedicated HCO beams in military Ka-band frequencies or on the standard wide area coverage beams which only use civil Ka-band frequencies.

An additional GX question that may soon be answered is the potential for a fourth backup satellite to be ordered. Inmarsat certainly has ample justification for placing a near term order, given its reliance on Proton launchers for all three GX satellites, and the run of problems that Russian rockets have had in recent months. Although Inmarsat would presumably portray an order as a sign of increased confidence in the market for GX, this would also add up to $200M of additional capex to the $1.2B GX program, even if no commitment was made to a fourth satellite launch at this stage.

Given Inmarsat’s more assertive stance in the market, it will now be particularly interesting to see whether Inmarsat can persuade distributors to share its positive view of the overall GX opportunity, and make revenue commitments similar to the $500M that Intelsat has achieved from Caprock, MTN and Panasonic for its EPIC system. Time will tell, but at least so far, my assertion last October that we had reached a turning point in MSS history has come only partly true: while it certainly appears that the next few years will bring regular price rises, an improvement in Inmarsat’s relationships with its distributors still seems like a distant prospect.

Permalink

« Previous Page — « Previous entries « Previous Page · Next Page » Next entries » — Next Page »

{kind=link}

{kind=link}

{kind=link}