04.08.13

The worst satellite public offering since Worldspace?

No I’m not talking about Intelsat’s current IPO! Although some might raise questions about the company’s debt levels, its also pretty clear that Intelsat’s mobility strategy and its high throughput Epic satellites are the envy of its FSS competitors. What I’m actually referring to is Row44, which went public at the end of January through a merger with Global Eagle, which had raised $190M in a blank check IPO. The end of year results from Row44 and Global Eagle have gone completed unreported, but were filed with the SEC last month, and highlighted just what a disastrous business Row44 really is.

In particular, as installations of the Southwest fleet neared completion, Row44′s revenues in Q4 dropped by 27% compared to Q3 (from $20.1M to $14.8M). Moreover, Row44 only generated total Internet connectivity revenues of $11.4M in 2012 while spending $19.6M on buying bandwidth from Hughes, and produced no revenues from its much ballyhooed content and portal services (despite spending $1.9M on video licensing fees).

{kind=link}

In 2013, Row44′s satellite connectivity commitment to Hughes will go up to a minimum of $28M (and more likely well over $30M, because of additional commitments made in early 2013 to add coverage in Russia, and additional trans-Pacific coverage planned later this year). Row44 has also changed its deal with Southwest, so it now only receives fees for passengers using connectivity (between $5 and $6 per user, while Southwest charges $8 for the service), rather than Southwest paying for every boarded passenger under the original agreement, and as part of the new contract, Row44 is adding more capacity, apparently to counter passenger complaints about “slow or restricted services”.

At an investor conference on March 13, Global Eagle’s CFO suggested that paid take rates for other providers “range from high single digits to high teens” and that inferences could be drawn from that for Row44′s take rates on Southwest. Of course that is completely untrue: take rates for Gogo are around 5%, and Global Eagle itself said back in November that the targeted take rate on Southwest was 6.5% in 2014, so its hardly likely that the take rate is higher than that today. I therefore have to wonder if Global Eagle’s CFO actually understands this business at all.

{kind=link}

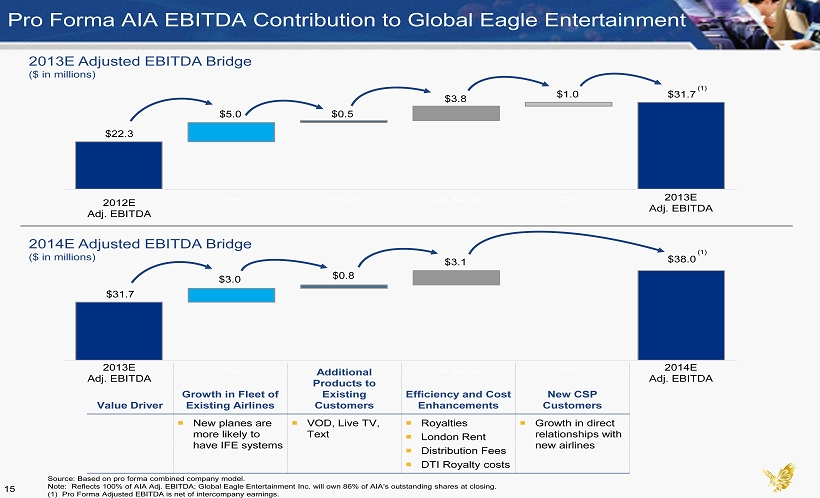

Indeed, the company seems to have a hard time predicting the outlook for its business even in the very short term: this March 13 presentation indicated that the 2012 adjusted EBITDA from Row44 and AIA respectively was -$26M and +$18M respectively, whereas on November 27, 2012, with just one month left in the year, Global Eagle forecast that the full year adjusted EBITDA results for Row44 and AIA would be -$25M and +$22.3M respectively.

{kind=link}

If we look forward to 2013, then it seems certain that Row44′s revenues will decline sharply, because of the slowdown in equipment installations (from $61M of equipment revenues in 2012 to ~$35M in 2013, and potentially to only $20M in 2014, based on Row44′s current business plan). More importantly, the company is set to make another significant loss on provision of connectivity services: I estimate $20M-$25M in revenues, depending on the take rates that Southwest achieves, compared to connectivity costs of well over $30M and more likely close to $40M (just in payments to Hughes, ignoring Row44′s own operational costs). In addition, content revenue is still minimal (Global Eagle described the product as “brand new” in mid March), with a very limited selection available, and by my estimate content and portal revenues will be no more than ~$5M this year.

In the longer term, Row44′s new deal with Southwest has locked the airline into a deeply unfavorable competitive position vis-a-vis JetBlue, who intend to offer Internet access for free. Southwest can’t possibly do the same, if they have to pay Row44 at least $5 for every passenger who uses the service, despite the two airlines competing very actively on other passenger amenities (like free checked bags). Moreover, if Row44 is ever to break even, it may have to cut back on the amount of capacity it buys from Hughes (rather than boosting capacity as Southwest currently plans), making Southwest’s Internet service even less attractive compared to JetBlue, which uses much cheaper Ka-band capacity.

In recent days, we’ve seen yet another report predicting rapid growth for in-flight connectivity deployment and revenues. However, none of these reports have got to grips with the issue of what services can be profitable for providers but still affordable for the airlines. Of course, if there’s one lesson to be learned from the Connexion-by-Boeing debacle, its that you can’t just assume companies will be able to continue providing service at an enormous loss indefinitely. After scraping through 2012, raising money at effective interest rates of up to 421%, Row44 has escaped for the time being by capturing Global Eagle’s cash balance. Perhaps unsurprisingly, given its management’s apparently tenuous connection to reality, Global Eagle now intends to “use its balance sheet” to pursue consolidation of the in-flight connectivity business, which might provide some relief from Row44′s current unsustainable business model, but on the other hand may simply drag down other companies in the sector.

We’ll be publishing our own detailed report on the in-flight connectivity business next month, which takes a very different approach to the analyses we’ve seen so far: instead of simply projecting how many planes might be fitted out with each technology, we’ll look at both the revenue and cost base of the various IFC providers, and discuss which of them may be able to find a sustainable long term business model.

TMF Associates MSS blog » Gogo’s bubble era IPO said,

June 12, 2013 at 4:25 pm

[...] not yet completed my forthcoming aeronautical communications market report, but I know a lot of people will be looking for some realistic numbers to value the company. So I [...]

TMF Associates MSS blog » Row44′s content strategy meltdown… said,

July 1, 2013 at 1:24 pm

[...] readers of this blog know, I’ve not been a fan of Row44′s content-focused strategy for inflight connectivity, and I pointed out how ludicrous Global Eagle’s forecasts were last [...]