06.12.13

Posted in Aeronautical, Financials at 4:25 pm by timfarrar

Gogo’s IPO roadshow is taking place this week (with completion apparently expected next Tuesday) after the company filed a revised S-1 on Monday June 10 indicating that it is seeking to sell 11M shares at between $15 and $17, giving the company an enterprise value (at the midpoint of this range) of approximately $1.3B (or even higher if you assume, as Gogo does, that the cash it raises needs to be spent on upgrading Gogo’s network to ATG-4, including doubling the number of cell sites by 2015). That seems pretty optimistic given the modest revenues that Gogo generates at present ($235M in 2012) and the losses that the company is making outside its well established Business Aviation segment.

I’ve not yet completed my forthcoming aeronautical communications market report, but I know a lot of people will be looking for some realistic numbers to value the company. So I decided to pull together my detailed estimates for Gogo through 2017, into a 21 page profile and analysis which I’ve published today. You can find a report summary and contents list here, and an order form here. And if you decide to buy my aeronautical market report when its available later this summer, you’ll receive a full credit for the price of the Gogo report.

Feel free to contact me for more details. As a taster, here’s the latest quarterly growth breakdown including 2013Q1. The last quarter is quite significantly short of my estimates, as despite the improving take rate trend line, Gogo took a significant hit on Average Revenue Per Session compared to 2012Q4.

UPDATE 6/13: And here is a comparison with the various analyst forecasts for Gogo which were given out at the roadshow. I’ve left off the names, to spare people’s blushes, but the bank that forecast this to be a $1.6B business in 2017 has clearly been drinking the same Kool Aid as Global Eagle.

Permalink

04.08.13

Posted in Aeronautical, Financials at 10:02 am by timfarrar

No I’m not talking about Intelsat’s current IPO! Although some might raise questions about the company’s debt levels, its also pretty clear that Intelsat’s mobility strategy and its high throughput Epic satellites are the envy of its FSS competitors. What I’m actually referring to is Row44, which went public at the end of January through a merger with Global Eagle, which had raised $190M in a blank check IPO. The end of year results from Row44 and Global Eagle have gone completed unreported, but were filed with the SEC last month, and highlighted just what a disastrous business Row44 really is.

In particular, as installations of the Southwest fleet neared completion, Row44′s revenues in Q4 dropped by 27% compared to Q3 (from $20.1M to $14.8M). Moreover, Row44 only generated total Internet connectivity revenues of $11.4M in 2012 while spending $19.6M on buying bandwidth from Hughes, and produced no revenues from its much ballyhooed content and portal services (despite spending $1.9M on video licensing fees).

In 2013, Row44′s satellite connectivity commitment to Hughes will go up to a minimum of $28M (and more likely well over $30M, because of additional commitments made in early 2013 to add coverage in Russia, and additional trans-Pacific coverage planned later this year). Row44 has also changed its deal with Southwest, so it now only receives fees for passengers using connectivity (between $5 and $6 per user, while Southwest charges $8 for the service), rather than Southwest paying for every boarded passenger under the original agreement, and as part of the new contract, Row44 is adding more capacity, apparently to counter passenger complaints about “slow or restricted services”.

At an investor conference on March 13, Global Eagle’s CFO suggested that paid take rates for other providers “range from high single digits to high teens” and that inferences could be drawn from that for Row44′s take rates on Southwest. Of course that is completely untrue: take rates for Gogo are around 5%, and Global Eagle itself said back in November that the targeted take rate on Southwest was 6.5% in 2014, so its hardly likely that the take rate is higher than that today. I therefore have to wonder if Global Eagle’s CFO actually understands this business at all.

Indeed, the company seems to have a hard time predicting the outlook for its business even in the very short term: this March 13 presentation indicated that the 2012 adjusted EBITDA from Row44 and AIA respectively was -$26M and +$18M respectively, whereas on November 27, 2012, with just one month left in the year, Global Eagle forecast that the full year adjusted EBITDA results for Row44 and AIA would be -$25M and +$22.3M respectively.

If we look forward to 2013, then it seems certain that Row44′s revenues will decline sharply, because of the slowdown in equipment installations (from $61M of equipment revenues in 2012 to ~$35M in 2013, and potentially to only $20M in 2014, based on Row44′s current business plan). More importantly, the company is set to make another significant loss on provision of connectivity services: I estimate $20M-$25M in revenues, depending on the take rates that Southwest achieves, compared to connectivity costs of well over $30M and more likely close to $40M (just in payments to Hughes, ignoring Row44′s own operational costs). In addition, content revenue is still minimal (Global Eagle described the product as “brand new” in mid March), with a very limited selection available, and by my estimate content and portal revenues will be no more than ~$5M this year.

In the longer term, Row44′s new deal with Southwest has locked the airline into a deeply unfavorable competitive position vis-a-vis JetBlue, who intend to offer Internet access for free. Southwest can’t possibly do the same, if they have to pay Row44 at least $5 for every passenger who uses the service, despite the two airlines competing very actively on other passenger amenities (like free checked bags). Moreover, if Row44 is ever to break even, it may have to cut back on the amount of capacity it buys from Hughes (rather than boosting capacity as Southwest currently plans), making Southwest’s Internet service even less attractive compared to JetBlue, which uses much cheaper Ka-band capacity.

In recent days, we’ve seen yet another report predicting rapid growth for in-flight connectivity deployment and revenues. However, none of these reports have got to grips with the issue of what services can be profitable for providers but still affordable for the airlines. Of course, if there’s one lesson to be learned from the Connexion-by-Boeing debacle, its that you can’t just assume companies will be able to continue providing service at an enormous loss indefinitely. After scraping through 2012, raising money at effective interest rates of up to 421%, Row44 has escaped for the time being by capturing Global Eagle’s cash balance. Perhaps unsurprisingly, given its management’s apparently tenuous connection to reality, Global Eagle now intends to “use its balance sheet” to pursue consolidation of the in-flight connectivity business, which might provide some relief from Row44′s current unsustainable business model, but on the other hand may simply drag down other companies in the sector.

We’ll be publishing our own detailed report on the in-flight connectivity business next month, which takes a very different approach to the analyses we’ve seen so far: instead of simply projecting how many planes might be fitted out with each technology, we’ll look at both the revenue and cost base of the various IFC providers, and discuss which of them may be able to find a sustainable long term business model.

Permalink

02.21.13

Posted in Aeronautical, Financials, Government, Inmarsat, Iridium, Maritime, Operators, Services, VSAT at 1:57 pm by timfarrar

As Inmarsat approaches its end of year results presentation, scheduled for March 7, the company’s stock price has been surging in the expectation of continued strong progress in the maritime market, which is likely to lead to full year wholesale MSS revenue growth for 2012 (excluding LightSquared payments) somewhat above Inmarsat’s 0%-2% target. This has been driven primarily by Inmarsat’s 2012 price rises, which have been so successful that Inmarsat announced further price rises of around 10% for E&E services last month.

I estimate that these new price rises could boost wholesale maritime revenues by a further $10M (roughly 3%) in 2013, on top of the pull-through from the mid year price rises in 2012, and as a result, it is plausible to imagine that Inmarsat’s wholesale MSS maritime revenues might rise by as much as 10% in 2013. Thus, unless there are severe cutbacks in government usage this year, overall revenue growth for 2013 may again come in quite a bit above the 0%-2% target. Our updated profile of Inmarsat provides full details of our forecasts by product, and will be released shortly.

That revenue upside perhaps explains why Inmarsat has become notably more aggressive in recent weeks, for example telling its sales team that commission will no longer be paid for selling Iridium products and services (historically Stratos has sold over $10M of Iridium equipment each year). In addition, the IS-27 launch failure appears to have given Inmarsat more confidence that potential partners will need GX for maritime and aeronautical services, rather than continuing to rely on Ku-band services in what may now become a capacity-constrained North Atlantic Ocean Region over the next couple of years.

One intriguing issue to watch in terms of Inmarsat’s relationships with its distributors is the ongoing dispute in Russia, where I’m told Morsviazsputnik has refused to pay for Inmarsat capacity for a substantial period of time (note that Inmarsat’s trade receivables have been increasing by about $10M per quarter during 2012, excluding LightSquared payments), unless all Inmarsat-equipped vessels going into Russian waters use a Russian SIM. This dispute has apparently extended to the Russians modifying their call routing gateway (which sends all traffic within 200 miles of Russian territory to an intercept point in Russia) to give them the ability to cut off the communications on foreign vessels. I’m told that in response Inmarsat has considered terminating the routing of traffic to the Russian intercept point, which would of course escalate the dispute even further and make it even more difficult to recover the withheld revenues.

Beyond this year, Inmarsat is guiding that its 8%-12% revenue growth in 2014-16 will be backend loaded, and so growth in 2014 will not need to increase sharply (which would be difficult prior to achieving global GX coverage). Indeed, a combination of continued price rises on L-band services and a release of some of the cash previously received from LightSquared (and never spent on installing filters) could help to meet expectations in the next few years, even if GX does not live up to Inmarsat’s projected $500M in wholesale revenue by 2019.

With respect to GX, I have been cautious about the $500M target because I have always assumed that maritime would account for the largest share of the GX business and it is very hard to see how Inmarsat could hope to generate $200M-$300M of wholesale maritime GX revenues by 2019, when Inmarsat itself estimates that only $145M was spent on maritime FSS space segment capacity in 2010.

However, I understand that Inmarsat is now suggesting that the GX government business will generate more revenue than the maritime market. Of course that is much harder to prove or disprove, especially as Inmarsat gave very little insight in the October 2012 investor day into whether the government business is expected to rely mainly on the dedicated HCO beams in military Ka-band frequencies or on the standard wide area coverage beams which only use civil Ka-band frequencies.

An additional GX question that may soon be answered is the potential for a fourth backup satellite to be ordered. Inmarsat certainly has ample justification for placing a near term order, given its reliance on Proton launchers for all three GX satellites, and the run of problems that Russian rockets have had in recent months. Although Inmarsat would presumably portray an order as a sign of increased confidence in the market for GX, this would also add up to $200M of additional capex to the $1.2B GX program, even if no commitment was made to a fourth satellite launch at this stage.

Given Inmarsat’s more assertive stance in the market, it will now be particularly interesting to see whether Inmarsat can persuade distributors to share its positive view of the overall GX opportunity, and make revenue commitments similar to the $500M that Intelsat has achieved from Caprock, MTN and Panasonic for its EPIC system. Time will tell, but at least so far, my assertion last October that we had reached a turning point in MSS history has come only partly true: while it certainly appears that the next few years will bring regular price rises, an improvement in Inmarsat’s relationships with its distributors still seems like a distant prospect.

Permalink

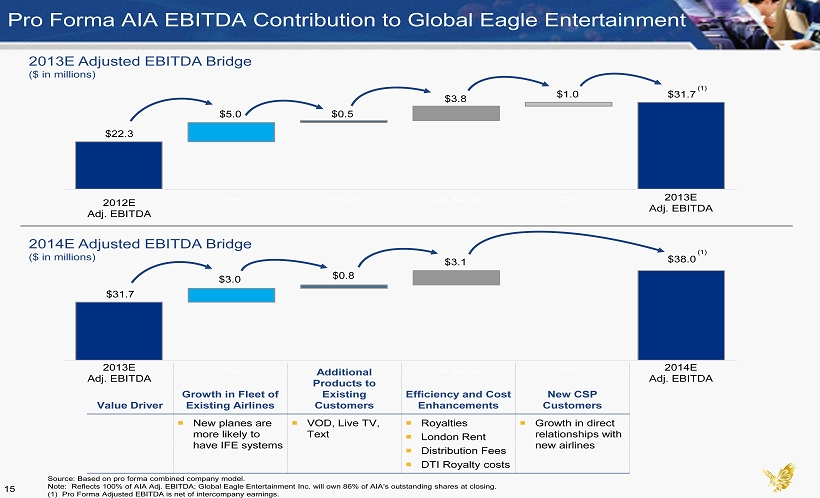

12.03.12

Posted in Aeronautical, Financials, Services at 4:45 pm by timfarrar

The latest Global Eagle investor presentation, which was filed with the SEC on November 27, makes for some pretty entertaining reading, much like the script for one of those Hollywood disaster movies that Row 44′s new owners may be fond of. Of course it requires some pretty convoluted logic to argue that Row 44, which is selling equipment at cost and losing money on every megabyte of data carried across its network, is worth $250M.

That’s especially true when the company fully intends to continue to sell equipment at cost and intends connectivity to be a “lower margin” service. In addition, despite a new contract with Southwest, which is expected to lead to a near 50% increase in connectivity revenue per passenger by 2014, the connectivity service is projected to produce less than $5M of gross margin (not EBITDA) that year. Instead, Row 44 and Global Eagle “believe the next frontier for growth will be providing quality entertainment, vast entertainment, first through the airlines into a projected multi-billion-dollar marketplace in the air” and so are projecting that Row 44 will make $49M of gross margin in 2014 from “TV/IPTV/VOD” and portal services.

What’s wrong with this picture? At its simplest, Row 44 is projecting that the take rate for connectivity on Southwest will grow to 6.5% (not outrageous, but perhaps ambitious given recent trends for Gogo and the predominantly leisure orientation of Southwest’s customer base) and the take rate for the “TV/IPTV/VOD” service will be 5.75% in 2014. Recall that passengers are paying $5 for internet connectivity on Southwest, which is the same as Row44′s assumed $5 per passenger fee for TV/IPTV/VOD. That’s all well and good if this was seatback IFE, available (and very visible) to all passengers with attractive early window content (very few people pay for live TV onboard planes in the US today), but remember that the only way to get access to the “TV/IPTV/VOD” service is through an Internet-enabled portable device.

Why on earth would almost as many passengers decide to pay (the same amount) for access to just the walled garden “TV/IPTV/VOD” service as pay for access to the rest of the Internet (where they might expect to have access to any content they choose – unless Row 44 decides to cripple the Internet service, which of course will lead to its own problems)? Will Row 44 have some incredibly compelling early-window content? Well studio executives apparently “Lol’d” when asked about whether they would allow early window content to be streamed over wireless IFE networks. And remember that while you might happily access email and social media on your iPhone, its far more difficult to watch long form video on a phone for an hour or two, so in reality even less devices may be suitable for watching the content services than for accessing the Internet.

Row 44 also intends to generate $19M ($0.15 per passenger carried) from its portal business by 2014, even though it has “only nominal revenue from the portal business today”. As another point of comparison, Row44 expects to make more than half of its passenger revenue from the video and portal services by 2014, when today Gogo only generates 2% of its Commercial Aviation revenue from “Gogo Vision, Gogo Signature Services and other service revenue” (i.e. video and portal services combined, plus other services such as VOIP for flight crews).

Fundamentally, I simply can’t understand why on earth Global Eagle think that this business is a good investment (though lack of understanding might be one reason). The history of inflight connectivity is littered with failures, and even Gogo, the market leader, is facing challenges in getting a return on its investment, let alone completing a successful IPO. In every respect, Row 44 is a worse business than Gogo: it has substantial ongoing bandwidth costs, far more expensive equipment, and (in Southwest) probably the least attractive airline in the US from the point of view of demand (few business travelers, short flights and no power outlets). I can only conclude that, as in the picture above, Global Eagle is suffering from the Icarus Syndrome, and flying too close to the sun for its own good.

Permalink

08.29.12

Posted in Aeronautical, Financials at 10:48 am by timfarrar

It seems that most if not all commentators have ignored Gogo’s Aug 14 S-1 amendment containing the company’s results for the first half of 2012, instead picking up on Gogo’s Aug 28 press release that Gogo has been approved to operate in Canada (which in fact according to Gogo’s SEC filing was actually approved back in mid July).

That’s a shame because the six month results are pretty fascinating: they show that in Q2 of 2012 Gogo’s take rate and (more significantly) the average revenue per passenger carried both fell compared to Q1. If the revenue per passenger carried does not grow after the price increases Gogo implemented during the second quarter of 2012, then this raises the question of whether we may already be close to the point at which Gogo’s average revenue per plane cannot be increased much further. In addition, Gogo’s average revenue per session fell from the previous year, despite the price rises. Gogo’s filing attributed the decline in revenue per session to more (lower revenue) sponsored sessions compared to the same period in 2011. However, this simply highlights that a major contributor to Gogo’s (rather modest) increase in take rates over the last year has been the growing use of sponsorships, which are counted as part of the “take rate” even when passengers do not pay anything to use the service.

The chart above shows how Gogo’s take rate has developed by quarter since its launch, and how much it has been driven by promotional activity, with take rates at an all time high during the Google promotion in Q4 2010, and falling quite sharply when there was very little promotional activity in Q2 2011. Q1 2012 saw another boost to take rates, again coinciding with high levels of sponsorship revenues.

Though there is clearly some underlying growth in the take rate, during the remainder of 2012 this is likely to be diluted by the increasing number of Gogo installations on regional jets (where usage is much lower than on longer flights) and the (more marginal?) deterrent effect of recent price increases. As a result, I now expect that barring some large scale sponsorship, Gogo take rates for 2012 as a whole are unlikely to exceed 6%, and if we only count paid usage by passengers, then the true take rate may remain below 5%.

That’s pretty scary given the $1B valuation supposedly being mooted for Gogo’s IPO and the $200M valuation put on Row44 in its recent fundraising transactions. Its also interesting that Gogo’s bankers insisted that their recent $135M loan should be secured against Gogo’s profitable Business Aviation subsidiary, with cashflows from that operation potentially devoted to pre-payments on the loan, so that their loan recovery would not depend solely on the success or otherwise of Gogo’s commercial aviation business.

Permalink

06.19.12

Posted in Aeronautical, Inmarsat, Operators, Services at 8:19 pm by timfarrar

That pretty much sums up the situation with inflight cellphone calls in the rest of the world, after OnAir’s CEO indicated that only 10% of OnAir’s inflight GSM traffic is now coming from voice calls. Just how disastrous a statistic that is can be discerned from the fact that Inmarsat’s total wholesale aero passenger connectivity revenue is only around $2M per year, from 160 planes equipped with cellular connectivity, or around $12K per plane per year (in fact the number might even be lower if Inmarsat is including the far larger number of long haul planes equipped with traditional seatback phones in its $2M total).

Grossing up to retail revenues, that means passengers are spending perhaps $30K to $40K per plane per year on cellular services, and so if only 10% of OnAir’s “traffic” (which I assume is measured in revenue terms) is derived from voice calls, then that is about $10 per plane per day in voice usage. Put another way, I estimate that on average there may be as few as 2 voice calls per plane per day!

For (a truly scary) comparison, take a look at OnAir’s estimates back in 2007, that Ryanair passengers would spend EUR300K per plane per year on voice calling, or 100 times more than the current level of usage.

Of course that shouldn’t really be a surprise, because the original providers of inflight phones in the US (Verizon Airfone and Claircom) both went out of business and Inmarsat’s revenues from seatback phones were about 2% of their original projection in the early 1990s. More recently, Ryanair also stopped providing inflight cellular services. Obviously the lack of privacy and the level of background noise make it pretty hard to conduct business on a cellphone call inflight, while the cost has generally been prohibitive for leisure users, and neither of those factors has changed in any meaningful way with the introduction of cellphone instead of seatback connectivity. As a result, its no wonder that business travelers much prefer email and SMS to voice calls, and some airlines have even decided to ban voice calling themselves, despite it being legal outside the US.

It therefore seems pretty ironic that we’ve had letterwriting campaigns to the FAA and FCC, a ban proposed in Congress and even a lobbying group set up by OnAir and AeroMobile, trying to argue that voice calls on planes are a bad or a good thing (depending on your point of view), when the reality is that almost no-one actually wants to do it anyway. However, just as with the title of this article, once people become convinced that there is no middle ground to the debate, logic tends to fly out of the window. In those circumstances, its no wonder that members of Congress are eager to get involved.

UPDATE (9/5): The FAA’s own consultation document on legalizing cellphone use onboard aircraft has now been published and gives some interesting specifics on the usage levels seen in other countries. In particular, the Brazilian regulator indicated that TAM was only seeing about 0.3 voice calls per flight leg, and the consensus of most respondent countries was “that there was relatively low use of cell phone voice communication on airplanes”.

Permalink

06.05.12

Posted in Aeronautical, Broadband, Inmarsat, Maritime, Operators, Services, VSAT at 12:45 pm by timfarrar

Without any hint of the PR blitz that I had expected, Intelsat has quietly updated its website to confirm my blog post in March, that it is about to order at least two new satellites, IS-29 and IS-33 to provide high capacity spot beam Ku-band service in the North Atlantic and Indian Ocean regions. These satellites will be in-service in 2015 and 2016 respectively, and are intended to “provide four to five times more capacity per satellite than our traditional fleet” with total throughput “in the range of 25-60 Gbps” (this appears to be a total not a per satellite figure – I would guess the throughput per satellite is around 12Gbps, roughly the same per satellite as Inmarsat’s GX, including its high capacity overlay beams).

UPDATE (June 7): Intelsat has now put out a press release and added more data to its website including a fact sheet, which states specifically that the throughput of 25-60 Gbps is per satellite. Obviously this figure is a wide range but it is clearly much greater than the Global Xpress per satellite capacity. I understand that one reason for Intelsat’s lack of publicity is the quiet period associated with its proposed IPO, but Intelsat definitely considers this a very important development and has been trumpeting it privately to distributors at its recent partner conference.

Intelsat is planning to integrate these new satellites into its existing maritime coverage as shown below (indeed there is less high capacity oceanic coverage than I expected, presumably because it will take time before Intelsat’s existing capacity fills up) and it appears that Intelsat will now be looking to compete head-to-head with Inmarsat’s Global Xpress as well as Viasat (both of which Intelsat appears to be referring to with its comment that “Unlike many new satellite operators, Intelsat is not constrained to Ka-band“)

What we haven’t yet seen are the details of Intelsat’s launch partners. It is clear that one partner is Panasonic, but the more important question is who Intelsat might have managed to secure in the maritime market. Inmarsat’s recent list of XpressLink distribution partners was notable for the absence of Vizada and most other major maritime VSAT providers, so if one or more of these maritime players now makes a substantial commitment to Intelsat, it will be another important sign that the transition to Ka-band in the maritime and aeronautical sectors is far from a foregone conclusion.

Permalink

03.24.12

Posted in Aeronautical, Financials, Services at 7:26 am by timfarrar

This week it was quite astonishing to see a Wall St Journal article hyping the in-flight passenger communications market in advance of Gogo’s planned IPO on NASDAQ, by highlighting incorrect statistics from In-Stat about the size of the opportunity. In particular the WSJ article states:

Currently about 8% of passengers use the service, up from 4% at the end of 2010, according to In-Stat, a research and consulting firm. That likely will reach 10% of passengers by the end of this year, In-Stat says.

Gogo’s amended S-1, filed on Wednesday, gives specific data for the take-rate on Gogo-equipped planes (nearly 90% of the market in the US), noting that it remained constant at 4.7% in both 2010 and 2011. Underlying usage is increasing, but the usage figures were distorted in late 2010 by a large sponsorship from Google (around $7M) which offered free access for 6 weeks between Thanksgiving and New Year. I’ve tried to back out the estimated quarterly evolution of Gogo’s revenues and take rate over the last three years, and as shown in the diagram below, the take rate at the end of 2011 was only just over 5%, and on current trends it will take several years to reach the 8% that In-Stat is wrongly suggesting is the take rate at present, let alone the 10% take rate In-Stat projects for the end of 2012.

Of course In-Stat’s projections of the in-flight communications market have been miles off all along. Last October, In-Stat claimed that “in-flight Wi-Fi revenue is expected to grow from about $225 million in 2011 to over $1.5 billion in 2015″. In reality, Gogo’s in-flight passenger WiFi revenues were just over $80M in 2011 and total passenger spending on in-flight connectivity services worldwide was only about $100M last year (most international services are supported by Inmarsat, who said on their recent results call that passenger connectivity generated between $2M and $3M of wholesale revenues in 2011). Surprisingly, Gogo even quotes an In-Stat forecast in its S-1 stating that “in-flight internet usage is expected to increase rapidly over the next five years, from approximately 15.6 million North American sessions in 2011 to 96.9 million by 2015″. However, with Gogo having only had 9M sessions in 2011, it is inconceivable that there could have been more than ~10M sessions in North America last year.

In this context, it is very surprising that the WSJ decided to quote In-Stat’s data without verifying it against the information in Gogo’s public filings. It is also worrying, with Gogo’s IPO set to take place in the near future, if potential investors take the WSJ article at face value and have a misleading impression about the current state of the in-flight communications market.

Permalink

03.15.12

Posted in Aeronautical, Broadband, Inmarsat, Maritime, Operators, Services, VSAT at 12:37 pm by timfarrar

The biggest news of this week’s Satellite 2012 show was only hinted at in the background, with many elements of the announcement (which I’m told was originally scheduled for Monday March 12) apparently delayed while the final details are worked out. Panasonic hinted at their role in this deal on the in-flight connectivity panel, stating that they would be investing “more than any other player in the aeronautical sector” in a new network, while Inmarsat backpeddled on their recent aggressive approach to potential Global Xpress partners, by indicating that they would allow GX maritime distribution partners to keep their own VSAT services rather than being forced to resell Inmarsat’s XpressLink Ku-band service for the next 2-3 years.

What has shaken up the industry is that Intelsat apparently planned to announce additional elements of their global Ku-band maritime and aeronautical service, using new spot beam Ku-band satellites in the Atlantic, Indian and Pacific ocean regions. Although Intelsat did issue a press release on Monday, highlighting their focus on mobility, this largely reiterated existing commitments, and omitted both new satellite plans (including IS-29, which is expected to be a high capacity satellite in the Atlantic, and will likely be built by Boeing) and Intelsat’s anchor tenant(s). More details on both of these elements are expected soon. Panasonic will apparently be the anchor aeronautical tenant for this new network and is expected to make an upfront commitment (for purchase of capacity) to help fund Intelsat’s satellite program which could exceed $100M. Many maritime VSAT providers are also looking actively at potential use of the network, as an alternative to Inmarsat’s Global Xpress project, because Intelsat have promised to operate purely as a wholesale capacity provider, rather than competing with their own customers as Inmarsat is doing. The cost of Intelsat’s Ku-band capacity is said to be comparable to Global Xpress (though that will undoubtedly be disputed by Inmarsat), and with Intelsat’s numerous Ku-band mobility beams, coverage will apparently be nearly as great as on Global Xpress.

The repercussions of this development are far-reaching, not least because it will make Inmarsat’s already challenging GX transition plan even more tricky. Inmarsat have recently backed off their original plan to select Rockwell Collins as the aeronautical terminal and distribution partner for GX and now appear poised to use Honeywell (who were originally Panasonic’s terminal development partner before Panasonic opted to bring that work in-house). Up until this week Inmarsat were requiring potential GX maritime distributors to drop their own VSAT service and instead act as agents for XpressLink until GX was launched, but Inmarsat’s CEO indicated on Wednesday that this is no longer the case. And Inmarsat are raising their prices for FleetBroadband service to try and prevent maritime VSAT competitors from using FleetBB as a backup, driving some of them such as KVH into Iridium’s arms with their new (and very aggressively priced) OpenPort backup service, which can cost less than 20% of Inmarsat’s on-demand FleetBB price per Mbyte.

Now the question is whether Inmarsat will have to engage in a further rethink of their maritime distribution strategy (prior to their hastily arranged maritime partner conference in May) as they look to assuage the widespread anger amongst distributors. Many distributors are openly delighted about Intelsat’s move, after they were told at Inmarsat’s January 2012 partner conference that they would just have to accept Inmarsat’s terms, and hand over their VSAT customers for XpressLink, because there was no other choice available. Inmarsat will also have to consider whether their revenue forecast for Global Xpress (of $500M in wholesale revenue by 2019 and $200M-$300M in 2016, based on their 8%-12% p.a. wholesale revenue growth target in 2014-16) is still achievable, especially if some of the key potential partners for maritime GX want to continue to use well-proven Ku-band services and therefore opt to stay with Intelsat for their maritime VSAT capacity.

Permalink

12.25.11

Posted in Aeronautical, Financials, General, Services at 6:42 am by timfarrar

Gogo has finally decided to strut its stuff, by filing an S-1 with the SEC in preparation for a potential IPO early next year. However, it needs to put on a very good performance over the next couple of years if this IPO is going to be successful.

The filing reveals some interesting statistics about the company, and highlights just how wrong most analyst forecasts for the passenger communications market have been. Bizarrely, the S-1 quotes Forrester projections that “in-flight internet usage is expected to increase rapidly over the next five years, from approximately 15.6 million North American sessions in 2011 to 96.9 million by 2015″ when the company knows that the 2011 number is simply wrong – Gogo (which had over 90% of usage in 2011) had “provided more than 15 million Gogo sessions” since its inception by the end of September, and previously stated at the beginning of this year that it had reached 10 million sessions, after the success of the free promotion with Google late last year (which itself generated 3 million sessions in 6 weeks). As a result, the total number of sessions in 2011 (when there hasn’t been the same level of promotional activity) across all providers in North America is certainly well below 10 million and more likely close to half the level estimated by Forrester. In fact the total number of sessions (free and paid) might be no higher in 2011 than in 2010 because of the distorting effect of the free promotion last year.

Perhaps one reason for quoting Forrester is that the other widely cited analyst projection (by InStat in October 2011) is even further off the map (one person deeply involved in the industry said to me that he “didn’t know what they had been smoking”), with InStat noting that “take rates have increased significantly, moving from an average of 4% in 2010 up to 7% in 2011” (contradicted by Gogo’s actual numbers showing no more than ~4% take rate in 2011) and that “in-flight Wi-Fi revenue is expected to grow from about $225 million in 2011 to over $1.5 billion in 2015” (again miles away from Gogo’s passenger revenues of $58M in the first 9 months of 2011).

However, now we have the public S-1 filing, perhaps some of these erroneous forecasts will come back down to Earth. The key data in the S-1 shows that current take rates are only about 4%, with users spending an average of $10 to $10.50 per flight, implying a severe (but unsurprising) skew towards laptop use on long flights (charged at $12.95). A survey (strangely citing data from 2009) showed that the average Gogo user had taken 14.2 domestic business flights in the last 12 months, indicating exactly as Connexion-by-Boeing found in 2006, that it is frequent business travelers who pay for in-flight WiFi and rarely anyone else. Of course, only about 10%-15% of airline passengers fly this frequently on business, so it is hardly surprising that current usage levels are so low (especially once very short flights are taken into account). It is also unsurprising that the service is dominated by repeat users (15 million sessions from 4.4 million unique users – and some of these unique users may have only used the service in late 2010, when free access attracted 2 million users in 6 weeks).

What is critical for the future growth of Gogo is therefore its ability to expand usage dramatically amongst leisure travelers and more occasional business travelers. The key statistic to watch is the average revenue per passenger, which has climbed from $0.32 in 2010 to $0.41 in the first 9 months of 2011. It would be useful to see in the roadshow how much of this growth is due to new leisure users (as opposed to growing awareness after major fleetwide rollouts were completed in 2010), e.g. by looking at the trajectory on Virgin America (which had fleetwide availability very early) and by examining more recent data on the average number of annual flights taken by a Gogo user.

If the average revenue per passenger (ARPP) only grows to say $0.50, because paid usage remains limited to frequent business travelers, then it will be hard for Gogo to generate more than about $100M in EBITDA by 2015, but if ARPP grows to say $1.00, then EBITDA could grow to ~$200M, due to the nearly fixed cost base of the ground-based system (airlines receive about a 15% revenue share at present, though this payment might be on a tiered system so could increase in the future if usage is higher). Clearly, to have a successful IPO at a value not less than the $500M invested to date, Gogo therefore needs to demonstrate convincingly how its ARPP can more than double within 2-3 years, which can only happen by achieving much greater take-up amongst leisure and occasional business travelers.

Permalink

« Previous Page — « Previous entries « Previous Page · Next Page » Next entries » — Next Page »

{kind=link}

{kind=link}

{kind=link}