12.20.13

LightSquared’s time machine…

As we head towards the holiday season, LightSquared’s attempts to find an alternative to being bought by Charlie Ergen are becoming ever more desperate, as the December 24 deadline to put forward an alternative plan approaches and the company takes a “time machine back to the summer…to formulate from scratch their own refinancing plan

…like the failed effort with Jefferies.”

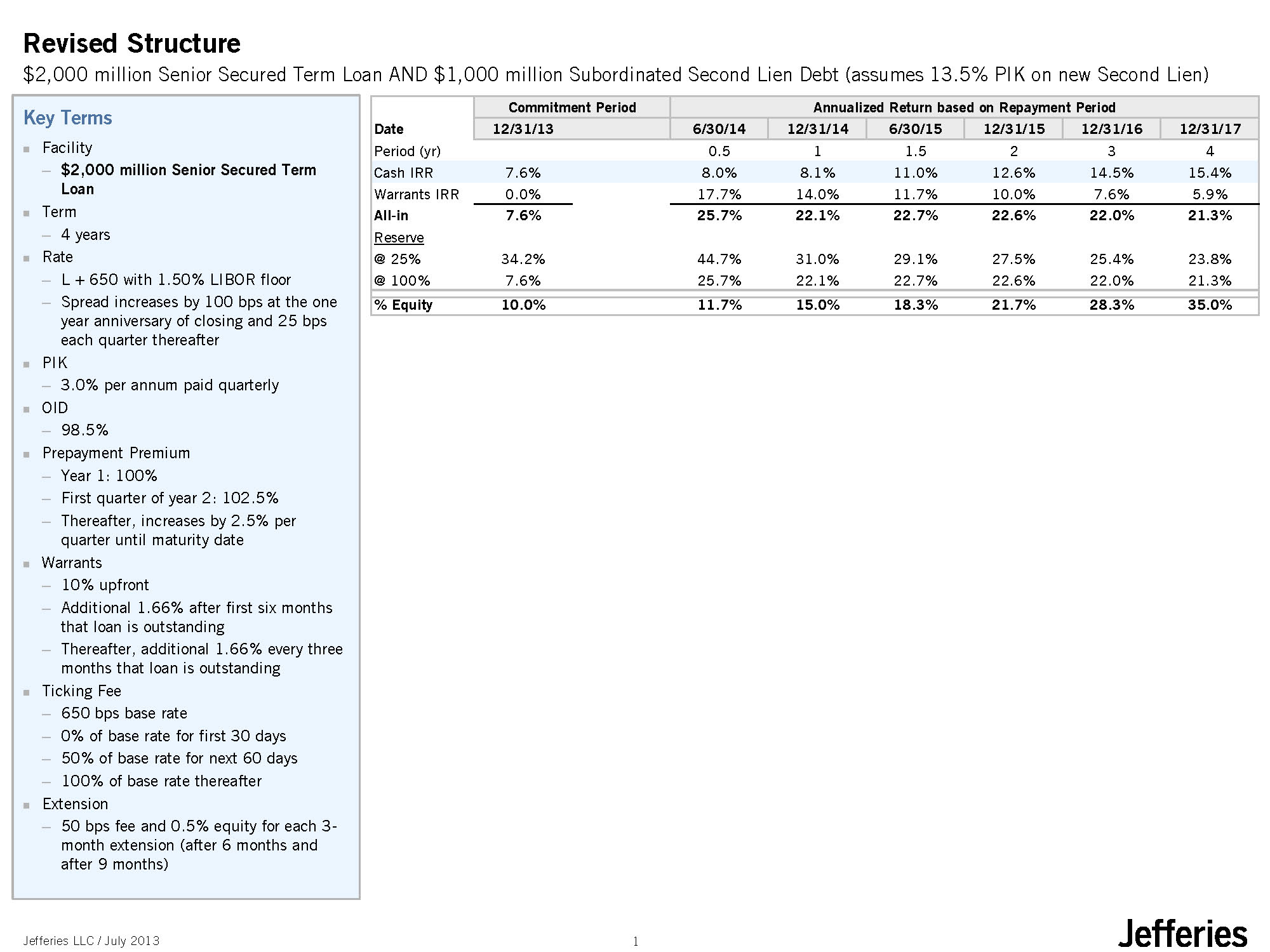

Reuters is reporting the terms of a $2B-$2.5B three year term loan to back a Fortress-sponsored exit plan as including 12% interest, all paid-in-kind, with an additional unspecified amount of equity injected into the company (presumably mostly achieved through rolling over existing investments). Unless a substantial amount of warrants are also included in this deal, the terms appear worse than those offered by Jefferies (and rejected by investors) back in July, which comprised mostly cash pay interest plus an ongoing ticking fee and substantial warrants.

{kind=link}

We find it hard to imagine that the judge will be happy with a proposal which involves waiting another 6-9 months for an FCC decision, with no certainty at the end of the process, and which would presumably result in DISH terminating its non-contingent cash offer. Remember that there are numerous other uncertainties in the near future as well, including the resolution of LightSquared’s Mexican coordination negotiations, the Cooperation Agreement with Inmarsat, LightSquared’s difficult relationship with the DoD (which led to the termination of a contract accounting for one third of LightSquared’s total satellite revenue earlier this year) and most importantly the unprecedented amount of spectrum that will be auctioned by the FCC in 2014 and 2015. All of these issues are discussed in detail in our new 49 page LightSquared profile, released yesterday – please get in touch if you are interested in purchasing a copy.

The AWS-1 auction in 2006 provides one good example of how large amounts of new spectrum coming to the market can have a major effect on the perceived value of spectrum. Take for example ICO’s July 2005 Offering Memorandum, which suggested its spectrum was worth $1.64/MHzPOP, whereas after 2006, ICO had to use an AWS-1 benchmark instead (in that case the most optimistic number that could be justified was $0.73/MHzPOP for the 20MHz F-block spectrum).

One of the underrated issues that is still to play out in the bankruptcy (and a key sticking point in negotiation of DISH’s proposed Asset Purchase Agreement) was that DISH’s bid included acquiring all of the litigation rights of the LightSquared estate. The most obvious effect that would have is on LightSquared’s lawsuit against Ergen for buying up its debt. However, it would also have significant consequences for the suit against the GPS industry and potential litigation against the FCC: whereas LightSquared soon may have nothing to lose by employing scorched Earth tactics, we suspect DISH would look for a compromise that would be acceptable to all parties. Finally, DISH could even sue Harbinger on behalf of LightSquared investors who lost money as a result of the “guarantees” that there was no GPS interference problem whatsoever.

We should soon know if this will be Phil’s last gasp, so just like the Delorean above, he will find himself “OUTATIME” or if we will have many months more of uncertainty about the FCC process. Either way, it looks like it is no longer FCC Chairman Wheeler who will have an unhappy Christmas, but instead it will be Judge Chapman, who is charged with resolving the LightSquared bankruptcy case and now has to determine just how much of LightSquared’s “alarming and reckless” efforts to fend off DISH she will tolerate.

chuckwagonttu said,

December 28, 2013 at 8:34 am

This is very interesting to watch play out. I appreciate all of your insights.

Any thoughts on where things stand with the Terrestar 1.4?

TMF Associates MSS blog » H-block auction: nearly done… said,

January 29, 2014 at 2:34 pm

[...] because of the low price of the H-block. That’s not unexpected (and indeed exactly what I predicted last month), but in my view DISH’s real asset value is in its potential “towers” (i.e. [...]